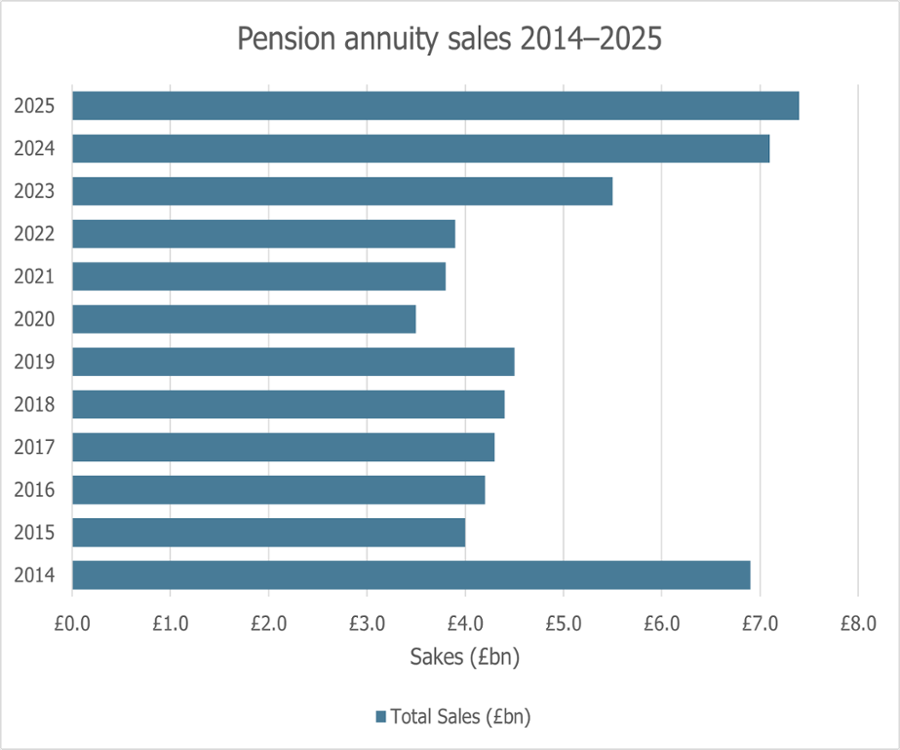

In 2014, the then Chancellor (and now podcaster), George Osborne, pulled a rabbit out of the Budget hat that nobody had seen coming. He announced the ending of the effective requirement for personal pension plans to be converted into an annuity in retirement. Osborne’s ‘pension freedoms’ came as a shock to pension providers and a near-death experience to insurance companies active in the annuity market. Share prices in the life assurance sector plummeted as the inevitable question was asked, “Who will buy an annuity now?”

As the graph shows, pension annuity sales fell from nearly £7 billion in 2015 to £4 billion in the following year, and then flatlined until recovering in 2023. That was when annuity rates recovered from historically low levels, thanks to an increase in long-term interest rates. The latest annuity sales figures, for 2025, have recently been released by the Association of British Insurers (ABI), showing that £7.4 billion was invested last year – £0.5 billion more than in 2014. Adjust for inflation – about 40% cumulatively since 2024 – and annuity sales are still well down in real terms.

The ABI data revealed some interesting trends:

The jump in higher value sales could be the first signs of a response to the plans to bring unused pension pots into the ambit of inheritance tax (IHT). From 6 April 2027, if death occurs on or after age 75, the effective tax rate on the unused pot could be 64% (40% IHT and then 40% income tax) or more. Faced with that level of tax and the associated complexities of managing income drawdown and the estate administration, an annuity offering guaranteed income for life (and no death benefit) has clear attractions. For a 65-year old, at present that income could start at over 5.25% and rise in line with the retail price index (RPI) inflation each year.

The value of your investment and any income from it can go down as well as up and you may not get back the full amount you invested.

Tax treatment varies according to individual circumstances and is subject to change.

The Financial Conduct Authority does not regulate tax advice.

If you believe we can help you with your finances please contact us: